- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Has SOL Bottomed Out? Multidimensional Data Reveals the True Picture of Solana

Original Article Title: Time to Call the SOL Bottom?

Original Article Author: blocmates

Original Article Translation: Ding Dang, Odaily Star Daily

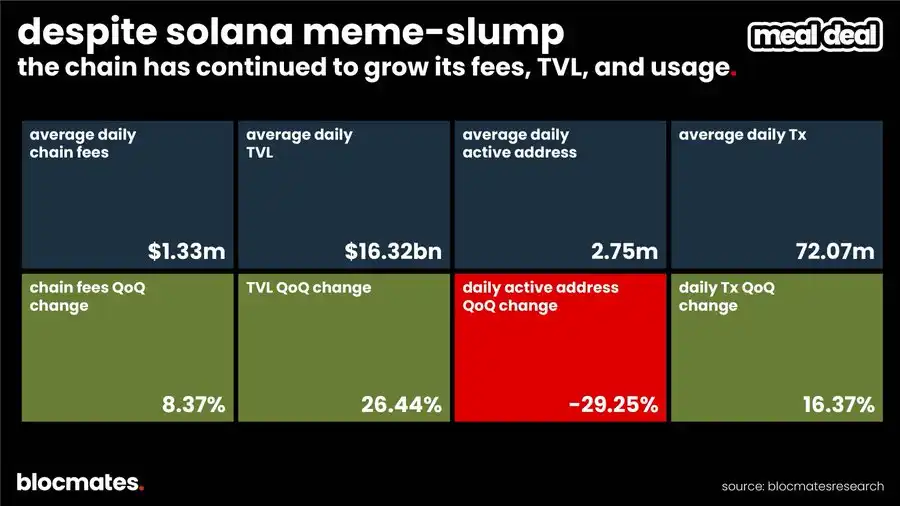

The third quarter of 2025 was a tale of two sides for Solana, all on the same chain. On the surface, the "Meme Downturn" brought about a significant cooling-off period: daily active addresses decreased, and Solana's user-centricity was gradually eroded by competitors. However, beneath the surface, the fundamentals of this chain became increasingly solid. The Solana core team continued to maintain a high frequency of iteration, driving forward one of the most ambitious technical roadmaps in the crypto industry; at the same time, its TVL grew by over 26% in the third quarter, and stablecoin supply almost tripled since the beginning of the year.

This report will systematically review the core technical upgrades that are defining Solana's future (such as Alpenglow, Agave), deeply analyze on-chain data performance, the health of ecosystem applications, and summarize our key insights on how Solana can solidify its position as the "default high-performance public chain."

Parallel Technical Innovations

While most users of the platform are busy chasing the latest meme emojis, the @solana core team has been advancing an ambitious set of system-level upgrade routes. This is not a patch-up of a single metric but a comprehensive system engineering effort to enhance network performance, security, decentralization, and user experience. These upgrades can be broadly categorized into three main types.

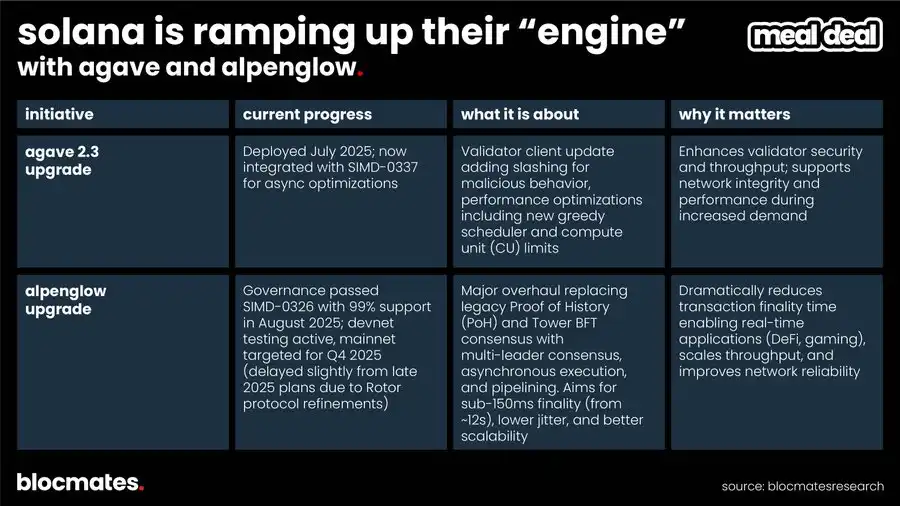

Category One: Core Engine (Consensus and Client)

This involves a fundamental transformation of Solana's "engine," aiming to enhance performance, speed, and security from the most basic level. Here is a great visualization chart, and if you're curious, you can learn more about the current staking ecosystem.

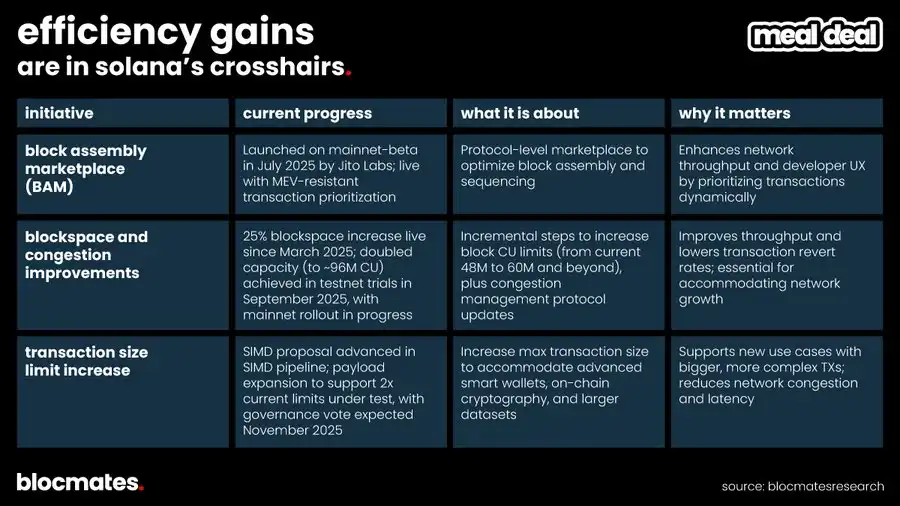

Category Two: Network Highways (Throughput and Efficiency)

The focus of this work is to widen the network "lanes" after enhancing the underlying performance, optimizing traffic scheduling to withstand future higher loads without congestion. If there is a hope for institutional users to truly onboard in the future, low latency and a stable experience are foundational, not optional.

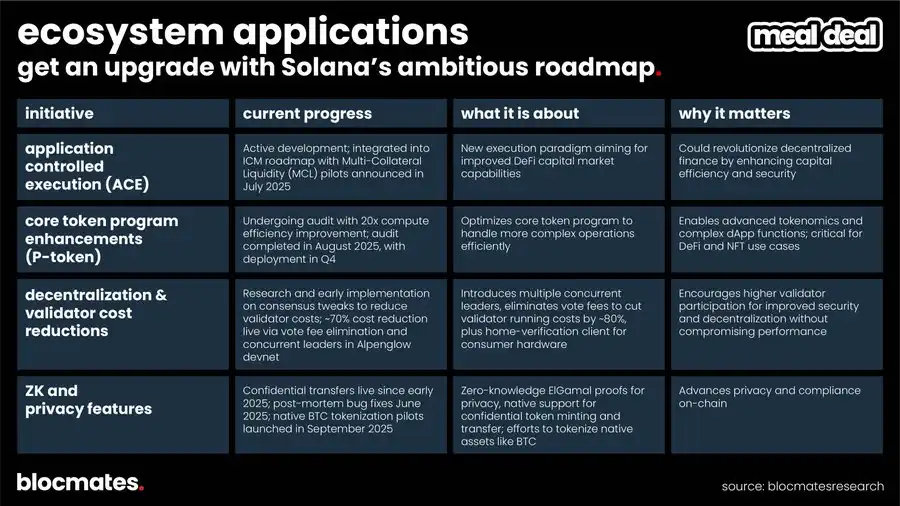

Category Three: Destination (New Ecosystem and Application-Layer Capabilities)

This category of upgrades is aimed at the most direct developers and end users, with the goal of providing more new features, supporting new types of application formats, and further enhancing the decentralization of the chain. In other words, this is the module that allows the "chain to do more."

Practical Impact of Technical Improvements

From a practical usage perspective:

· Alpenglow: Sub-150ms final confirmation speed enables retail users to use high-frequency DeFi, gaming, or micropayment applications on-chain, with performance approaching the levels of Binance (100ms) and Aptos (200ms).

· Firedancer: Potential capacity exceeding 1 million TPS far surpasses Ethereum and its L2 solutions (such as OP's ~2k TPS), Sui's 300k TPS, and centralized exchanges (Coinbase peaks around 500k TPS). It also significantly reduces systemic risks of single-client failures (Ethereum's Geth still accounts for 60% of nodes).

· Block Space Improvements, Congestion Alleviation, and Transaction Size Limits Optimization: Enhancing the overall experience of using the chain, enabling finer-grained microtransactions, ICOs (like $PUMP), and fast transactions, while reducing failures due to congestion.

· Decentralization and Node Cost Reduction: Allowing users with lower technical barriers to run nodes, thereby enhancing the security and decentralization of the entire network.

· ZK and Privacy Support: Providing a compliant, private, and secure foundation for the entry of RWAs and institutional users.

· BAM (Fair Trades, MEV Resistance): Ensuring transaction fairness and protecting users from MEV losses, making the on-chain experience closer to an expected low-cost CLOB environment.

· ACE (Multi-Collateral Liquidity Event): A further push to deepen the DeFi capital markets, enabling them to compete with platforms like Aave, and support more complex financial instruments.

PUMP ICO: On-chain Stress Test Validation

In July 2025, Pump.fun's ICO served as a real "stress test" to validate Solana's performance. @pumpfun managed to raise $500 million and $1 billion through on-chain and centralized exchange in just 12 minutes, reaching a valuation of up to $40 billion. During the event, 3,878 investors transparently participated in the purchase on Solana's DEXs like Raydium and Jupiter, while some CEXs (such as Bybit) experienced delays due to API failures, causing approximately 2,500 confirmed contributors to miss out on placing orders promptly and necessitating refunds.

Does this signify that we are witnessing a potential future scenario where the performance of decentralized blockchains begins to surpass that of centralized exchanges?

So, Where Does Solana Stand Now? The Truth Revealed by Data

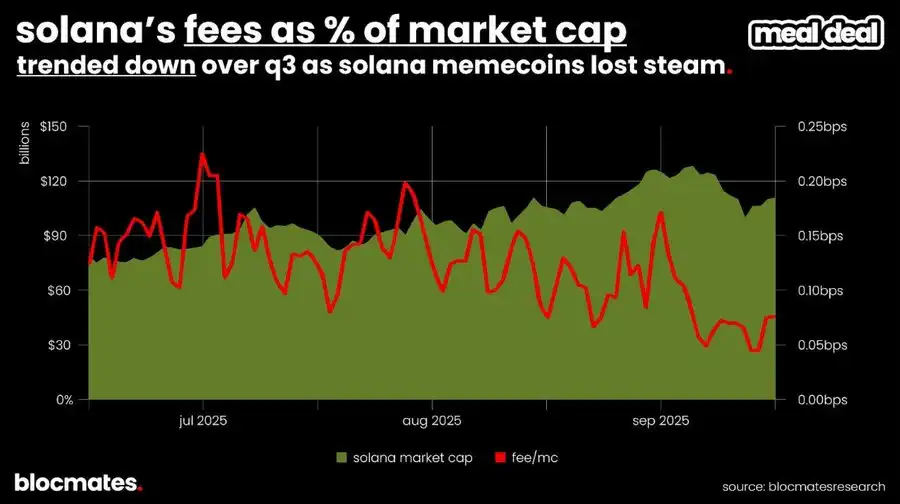

From a data perspective, as traders shift from meme speculation to perpetual contracts, Solana's on-chain revenue metrics have been significantly impacted: the on-chain fees as a percentage of SOL's market cap have dropped by over 60% since the July peak.

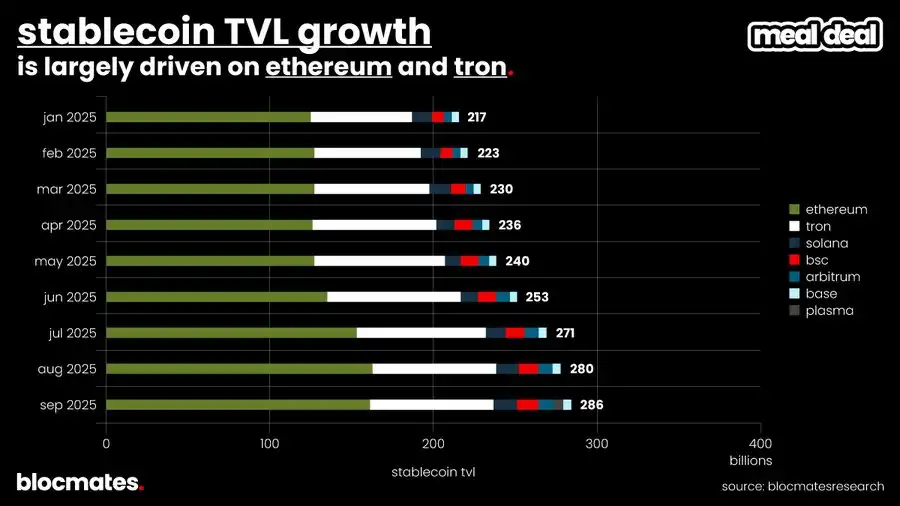

Meanwhile, despite the ongoing discussions of stablecoins on Capitol Hill and Wall Street, the leaders remain Ethereum and Tron, with Solana alongside Base, BSC, Arbitrum, and other chains in the "second tier."

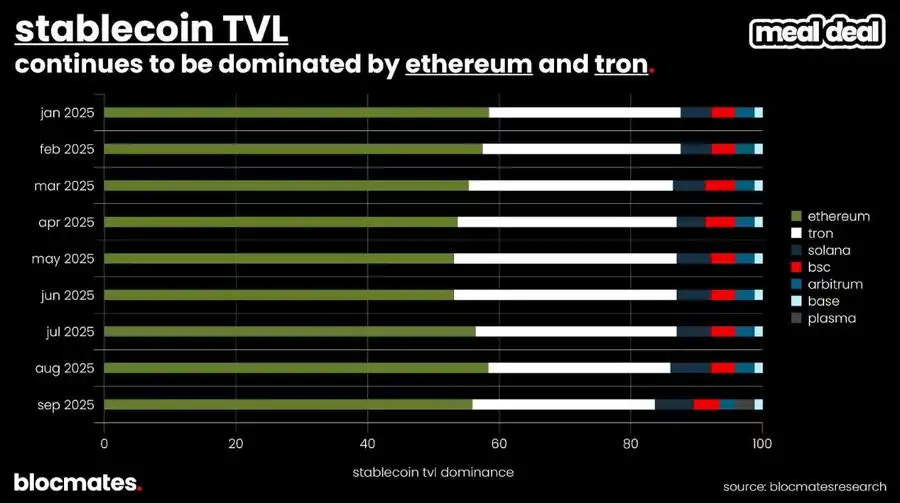

Further dissecting the stablecoin TVL share reveals that Ethereum and Tron have nearly always dominated over the past few quarters, while some emerging application chains—such as @Plasma—have started gradually breaking into this landscape.

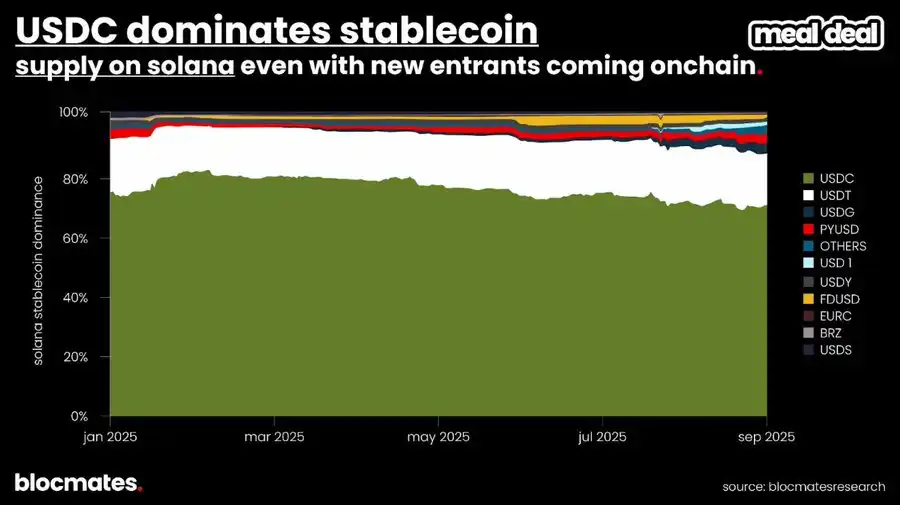

Nevertheless, Solana still provides a fast, low-cost, and liquid USDC usage environment, which may be why Western Union chose to build its stablecoin business on Solana.

“Experimental” will be one of the core themes of this report, and this spirit is also reflected in the stablecoin ecosystem: new projects are gradually eroding USDC's dominant position, bringing more competition to the Solana stablecoin landscape.

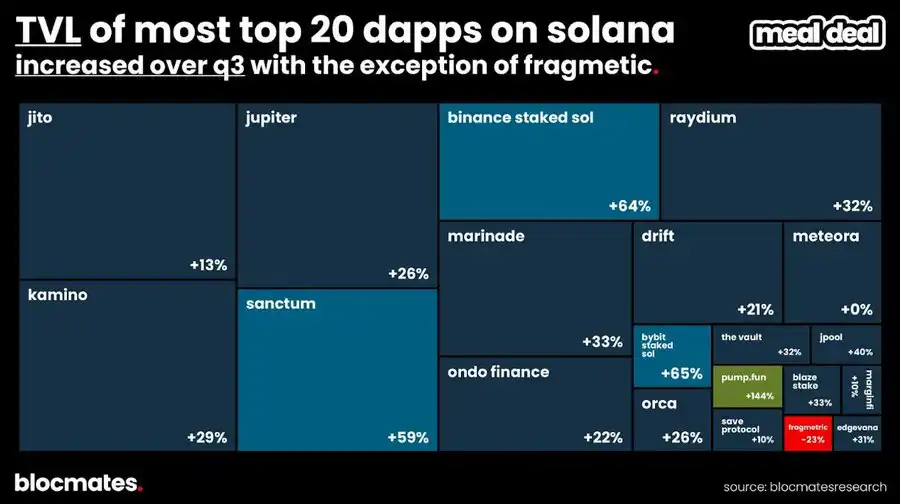

Which ecosystem participants are driving chain growth?

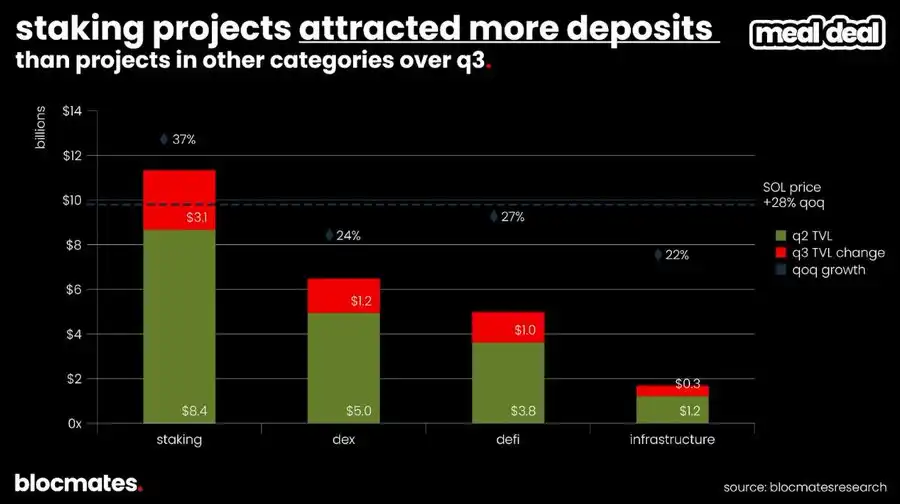

From the TVL growth perspective, staking products were an absolute highlight in Solana's third-quarter applications, with Binance and Bybit's staking of SOL and @Sanctumso's products all seeing over 50% growth in the third quarter.

In contrast, DEX, DeFi, and infrastructure products, although TVL has also risen, have not surpassed SOL's own 28% increase—meaning that in terms of SOL valuation, these categories were actually net outflows in the past quarter.

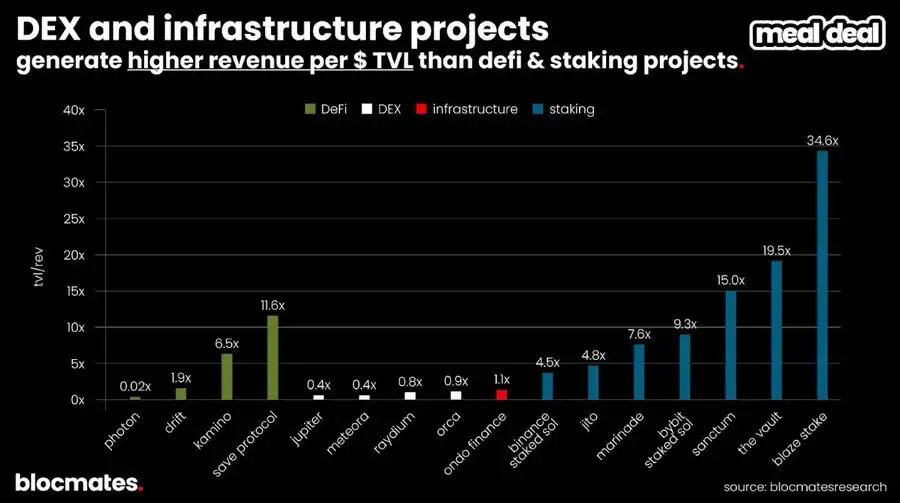

The downside of staking products is their weaker profitability: on average, a staking protocol needs 21.7 times the TVL to reach the average revenue level of DEX in this sample. This once again demonstrates a fact— in the crypto world, speculators contribute far more profits than savers.

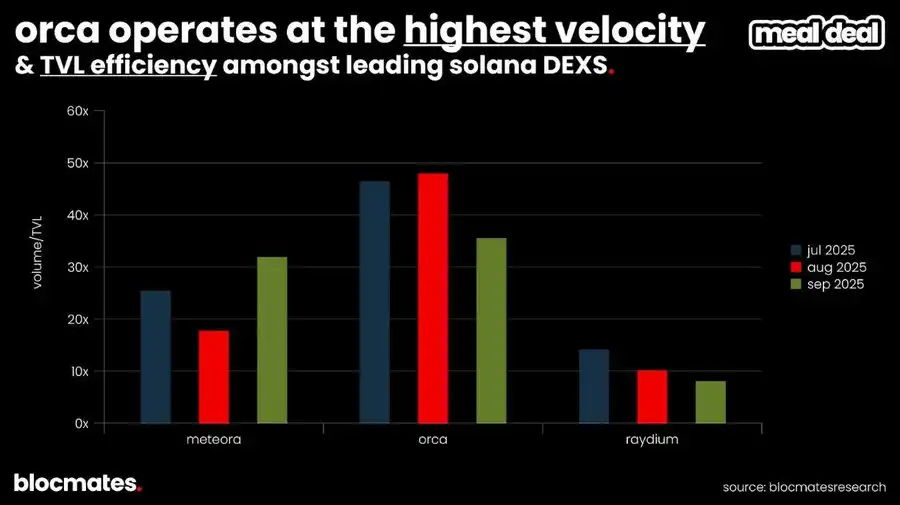

In the DEX race, @Orca_so has always maintained a leading position in TVL efficiency (i.e., “trading speed”). For a given level of liquidity, Orca has the highest trading frequency per dollar.

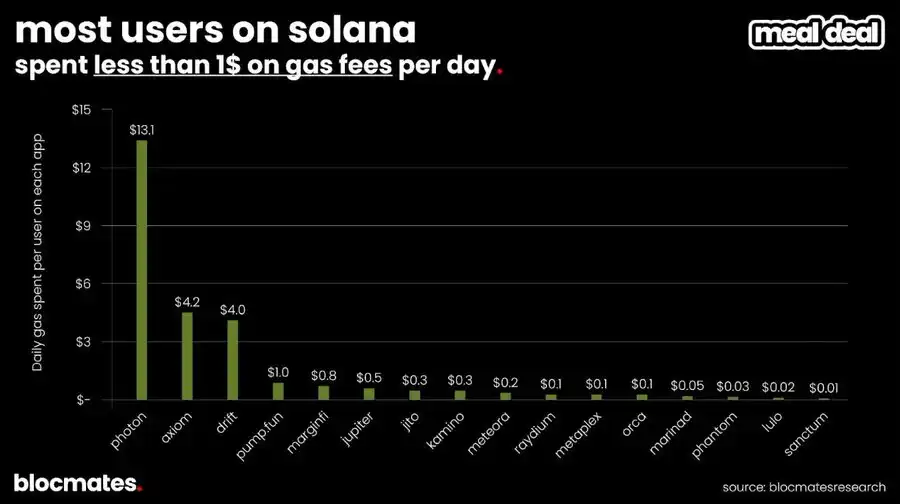

While Solana has always been known for being "fast and cheap," that doesn't mean there are no exceptions. For example, some high-frequency power users have found that their average daily fees on trading platforms like @tradewithPhoton or @AxiomExchange far exceed expectations.

However, for the vast majority of users, using the most common applications on Solana costs only a few cents a day.

Comparison of Solana and Core Competitors

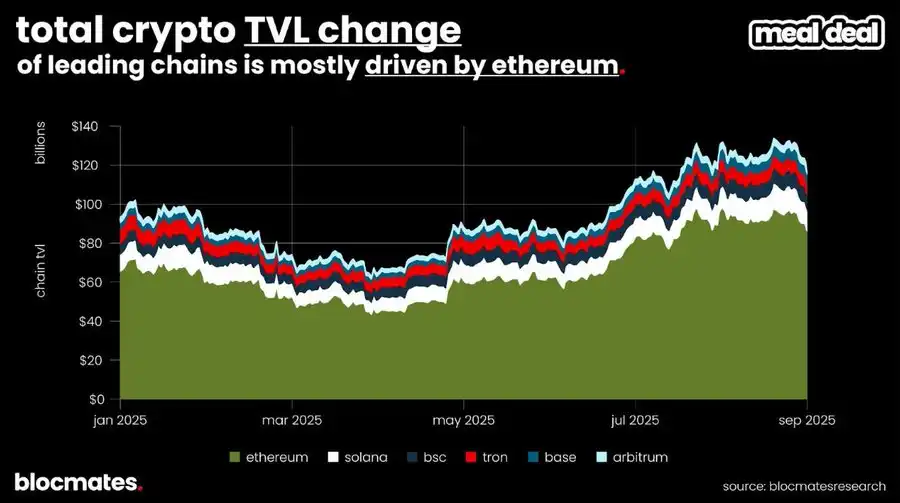

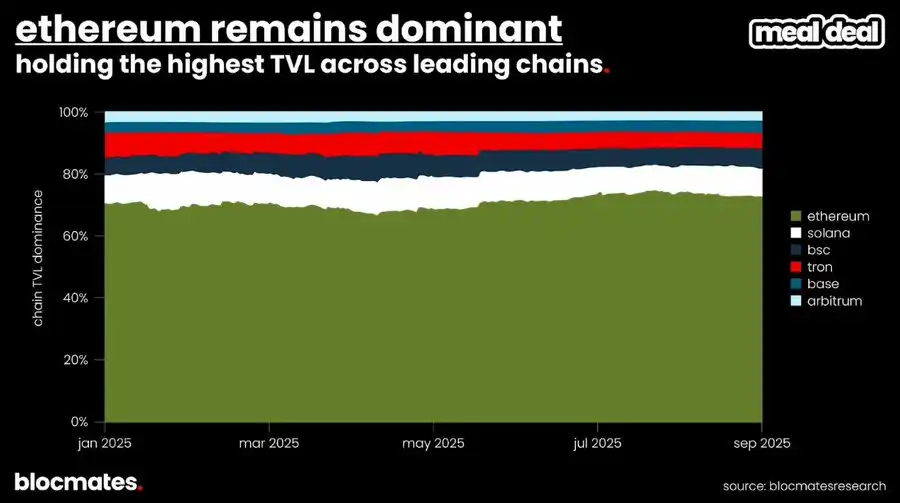

Total Value Locked (TVL) was slightly below the historical high of nearly $180 billion in 2021 at the end of the third quarter. However, when comparing the various competing public chains, the quarter-on-quarter TVL changes are actually quite limited.

The market share chart below clearly shows how the TVL of these competitors fluctuates in sync each week. As Newton said, "Capital, if not idle, is often idle," and once capital is entrenched, large-scale migration is often difficult to achieve.

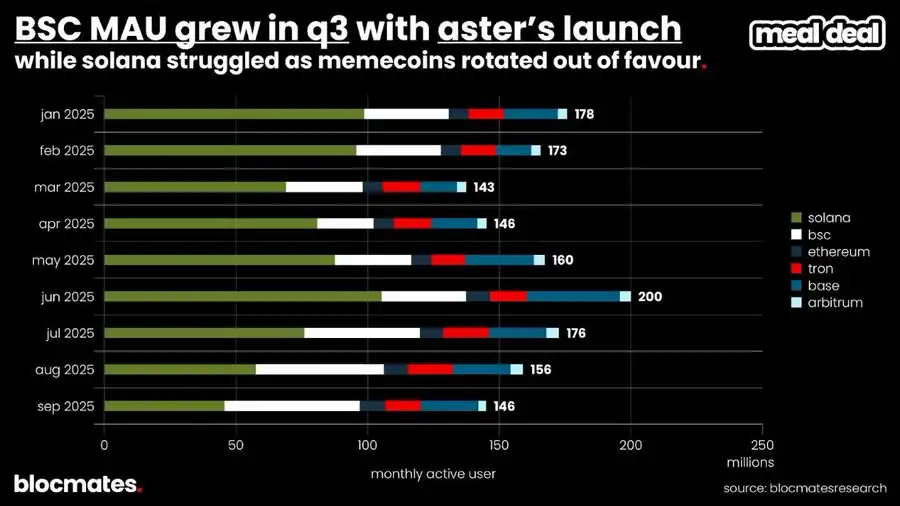

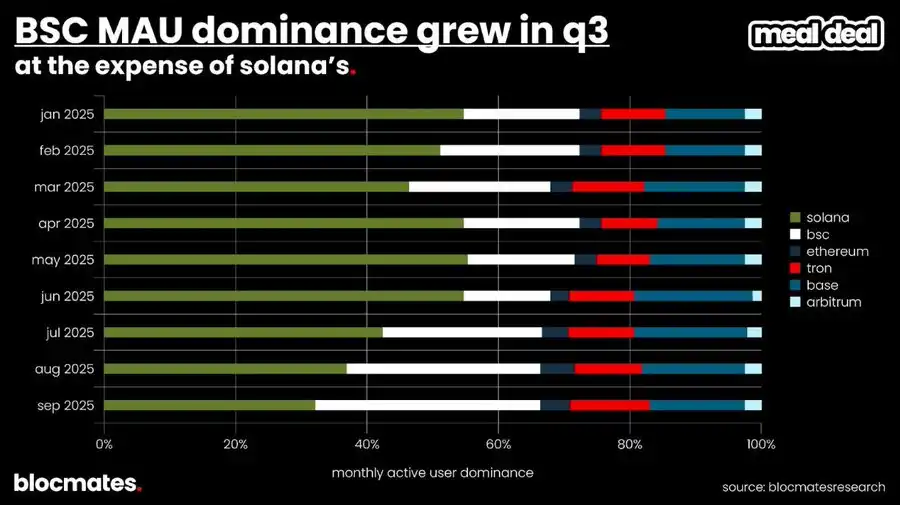

In terms of user base, Binance Smart Chain captured the most attention in the third quarter with a perpetual DEX linked to CZ—Aster. Many users either chose to exit in early summer or migrated from Base and Solana to BSC.

While Solana saw significant user growth in the second quarter, its share also declined in the third quarter, almost in sync with the waning market interest in meme trading.

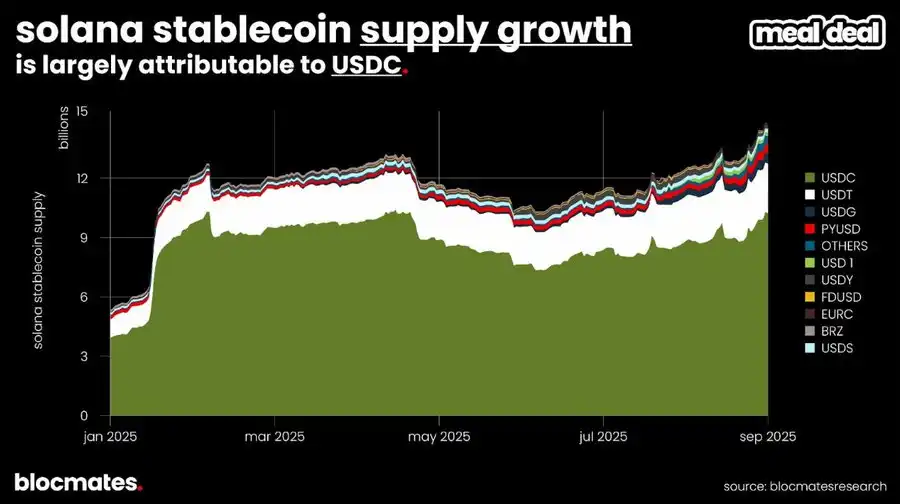

However, it is worth noting that due to the surge in interest in stablecoins, Solana's stablecoin supply almost tripled from the beginning of the year to the end of the third quarter. Indeed, "fast and cheap" is a major selling point to attract users to use stablecoins, especially against the backdrop of Solana's mature DeFi ecosystem.

While these metrics paint the current picture, they do not necessarily reflect the future direction. Solana's identity has always been that of an "experimental chain." To understand the future use cases and narratives, we must observe where funds are flowing into new experiments.

VC Fund Flows: Which Projects Are Getting Funded?

Here are some Solana projects that received funding from notable institutional investors in the third quarter:

· @raikucom: Completed a $13.5 million seed round in September 2025, focusing on real-time liquidity scheduling and cross-chain bridging on Solana. It caters to high-frequency trading applications, supports sub-second settlement, and mitigates MEV risk. The round was led by @PanteraCapital, and the funds will be used for mainnet upgrades and further integration with DEXes like @JupiterExchange.

· @bulktrade: Closed a $5 million seed round in August 2025, offering an institutional perpetual DEX that emphasizes gasless batch execution, with single trades of up to $10 million. The round was led by @robotventures and @6thManVentures, with Solana co-founder @aeyakovenko participating as an angel investor. Its alphanet testnet went live in the third quarter.

· @meleemarkets: Concluded a $3.5 million pre-seed funding round in July 2025, combining DeFi with social prediction in a gamified prediction market protocol where users earn rewards through accurate predictions. The round was led by @variantfund and @dba_crypto, with the funds allocated for oracle integration and mobile app launch. The project secured the second position in the Solana Breakout Hackathon.

· @hylo_so: Wrapped up a $1.5 million seed round in September 2025, presenting a decentralized stablecoin protocol on Solana that issues yield-bearing stablecoins (e.g., sUSD) through overcollateralization and an auto-rebalancing mechanism. The round was led by @robotventures, with participation from @SolanaVentures. The funds will be used for mainnet deployment and integration with lending platforms like @Kamino.

Where Are the Opportunities and Risks?

In the third quarter, Solana displayed a state of "breakthrough with challenges." On one hand, innovative applications are continuously approaching product-market fit, and Digital Asset Treasury (DAT) companies are also shining brightly; on the other hand, the entire ecosystem has had to face some tricky issues.

Standout Projects in Q3

Among the numerous dApps that emerged in this quarter, the following projects that have gone live are particularly notable:

· @Titan_Exchange is a new DEX aggregator launched in Q3, utilizing an improved algorithm to extract depth from different liquidity pools with machine-level precision to obtain the best price, outperforming existing similar products in 80% of cases.

· @DefiTuna is a new DeFi AMM launched in Q3, integrating a true on-chain limit order mechanism directly into the AMM design, avoiding security risks associated with off-chain matching and allowing LPs to leverage their liquidity positions up to 5x (leveraged yield).

· @xStocksFi tokenizes stocks custodied by a licensed broker, enabling crypto users to easily access the economic rights of their underlying stocks; it launched in early Q3, with a single-quarter trading volume exceeding $800 million and a market share of approximately 60%.

· Pump.fun (streaming + mobile) initiated a token buyback in Q3 and relaunched its live streaming feature after facing significant selling pressure previously, with a cumulative buyback size reaching $1 billion by the end of the quarter.

· @MetaDAOProject made headlines due to large-scale oversubscribed projects such as Umbra. Projects launched through MetaDAO will have legal, economic, and governance rights embedded in their tokens, known as "ownership coins." Additionally, its governance proposals are not decided by voting but by pricing through "futarchic markets," allowing participants to express their views with real money.

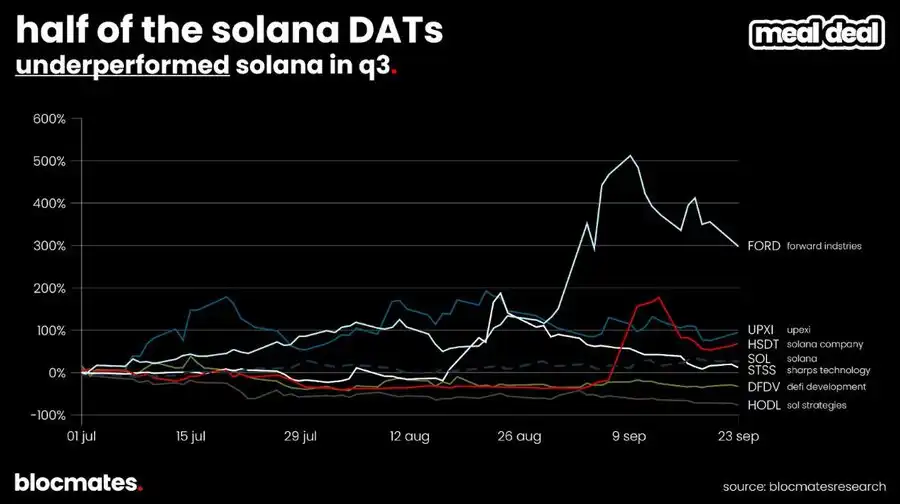

DAT Development Update

In Q3, Solana's DAT in the ecosystem raised approximately $4.25 billion through private placements, PIPEs, and equity issuances, with Forward Industries (FORD) being the largest; around $3.5 billion was used to purchase 14.5 million SOL, accounting for 2.3% of the circulating supply of SOL.

However, Solana DAT still couldn't escape the mNAV contraction pressure that was prevalent in the third quarter of the crypto DAT ecosystem.

Addressing Common Criticisms

Like almost all crypto projects, Solana itself is in a continuous evolution phase and is far from perfect. From our perspective, the following criticisms are more of growing pains in the process of maturation but are still worth noting.

Main Risk: Brand Narrative

Solana's longstanding tag has been "the best place for experimentation." Trading bots, ICM, consumer apps, AI agents—where did these innovations first emerge? Solana.

However, in this cycle, attention has become increasingly scarce, and projects that find product-market fit seem to only focus on a few tracks and very few applications. This stagnation has allowed competitors to seize the narrative:

· Perpetual contracts have migrated from applications on a general chain to applications specialized chains like Hyperliquid;

· Base, through Base app and Zora, has deeply bet on the consumer app narrative, an area that was once Solana's strength;

· Stablecoin chains like Tempo, Plasma, Stable, Arc continue to threaten Ethereum and Tron's stablecoin dominance.

This also leads to the core risk: yes, Pump is a revenue machine and has indeed resisted competition from the "external" (Base/BSC) and "internal" (BonkFun), but the unintended consequence of this success is the potential for Solana's brand to be permanently locked into a "casino chain" narrative.

To reverse this trend, Solana must drive a new narrative. Perhaps the answer is still Pump, but through its live platform; perhaps it is the "exit-scam-proof ICO" and new governance structure proposed by MetaDAO; or maybe it is Toly's experimental approach with a personal touch, targeting Hyperliquid. The ecosystem needs a new story that can dilute the stigma brought by "sub-second holding retail investors."

Our Outlook on Solana's Future

Despite a slight market downturn following the end of Meme Season, the significance of short-term price fluctuations is diminishing. Solana has established a strong position and is poised to endure in the long term.

The newly launched high-performance blockchains (such as Sui, Aptos, Sei) have not posed a substantial threat to Solana as they did in the previous cycle when Solana challenged Ethereum. Even though some competitors may have stronger theoretical technology, Solana is already "fast enough, cheap enough," offers a good user experience, and supports a large ecosystem.

Technical capabilities and smooth user experience are the foundation of adoption. Solana is not resting on its laurels but is continuously iterating rapidly (as detailed in the earlier upgrade section of this report) to solidify its position and expand its capabilities. For these reasons, developers still consider Solana their preferred high-performance option, and we believe this trend will not reverse.

Solana embodies the spirit of the crypto space – "daring to try, open competition, extreme market orientation" – and is the best arena to validate product-market fit. Regardless of where this cycle leads, Solana has the prerequisites to survive and continue to thrive. Even though some transaction volumes may flow to application-specific chains, we still believe Solana will maintain its leading position in the general-purpose chain space.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.